Australia Endoscopy Devices Market Size, Share, Report 2026 2034

- Market Research Insights

- Jun 8

- 6 min read

Market Overview

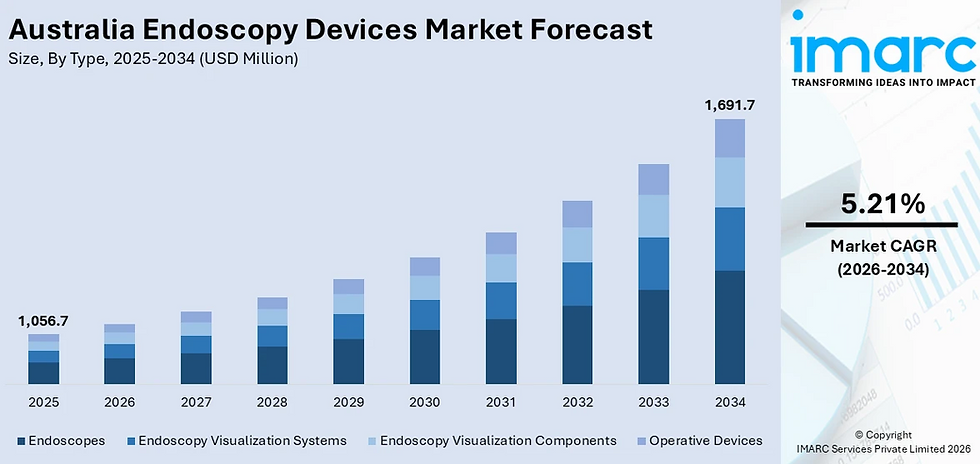

The Australia endoscopy devices market is witnessing strong growth due to advances in medical technology and increasing demand for minimally invasive surgeries. The market size reached USD 1,056.7 Million in 2025 and is projected to reach USD 1,691.7 Million by 2034, exhibiting a compound annual growth rate (CAGR) of 5.21% during 2026‑2034. Growing healthcare awareness and emphasis on cost‑saving treatments are adding momentum to the market, while the increasing proportion of elderly people and the rising incidence of chronic conditions are also driving demand for endoscopic treatments.

This market is strategically important to Australia’s medical technology and healthcare economy, supporting early disease detection, minimally invasive surgical interventions, and improved patient outcomes. Australia is experiencing a rising incidence of gastrointestinal disorders and chronic conditions, notably colorectal cancer, which is projected to be the fourth most commonly diagnosed cancer in 2024 with an estimated 15,542 new cases. National programs such as the Bowel Cancer Screening Program reinforce the trend by advocating regular screening and preventive care, driving adoption of endoscopic products throughout urban locations and regional health networks.

The Australia endoscopy devices market is poised for sustained expansion, driven by chronic disease prevalence, technological innovation, and government healthcare investment. With a projected CAGR of 5.21% through 2034, the market presents significant opportunities for manufacturers focusing on AI‑powered diagnostics, high‑definition imaging, and robotic‑assisted endoscopy systems.

AUSTRALIA ENDOSCOPY DEVICES MARKET SUMMARY

The Australia endoscopy devices market encompasses a range of medical devices including endoscopes, visualization systems, operative devices, and accessories used for diagnostic and therapeutic procedures across gastrointestinal, respiratory, urological, and other medical specialties.

The ecosystem spans medical device manufacturers, hospitals, specialized clinics, research institutions, and government healthcare programs.

Major segments identified in the endoscopy devices industry include type (endoscopes, visualization systems, operative devices, accessories), application (gastrointestinal endoscopy, laparoscopy, arthroscopy, urology endoscopy, bronchoscopy, others), end use (hospitals, ambulatory surgical centers, specialty clinics, others), and region (Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia).

Key trends shaping the market include rising prevalence of gastrointestinal and chronic diseases, technological advancements in endoscopic equipment (HD imaging, 3D visualization, robotic‑assisted endoscopy, AI‑powered diagnostics), and government healthcare support and infrastructure investment.

PORTER'S FIVE FORCES ANALYSIS – AUSTRALIA ENDOSCOPY DEVICES MARKET

The competitive dynamics of the Australia endoscopy devices market can be analysed using Porter's Five Forces framework.

Bargaining Power of Suppliers – Moderate

Endoscopy device manufacturers rely on suppliers of specialized components, optical systems, imaging sensors, and consumables. The technical expertise required for high‑definition imaging, 3D visualization, and robotic‑assisted systems gives established component suppliers moderate leverage. However, ongoing collaborations between medical device companies and research institutions promote local development and integration of advanced technologies.

Bargaining Power of Buyers – Moderate

Australia's public hospital networks, private healthcare providers, and ambulatory surgical centers represent concentrated purchasing channels that negotiate volume‑based contracts for endoscopy equipment. Government funding for public hospital equipment adoption and regional health programs supports procurement, while healthcare providers increasingly seek cost‑effective, high‑precision devices.

Threat of New Entrants – Moderate

Significant capital requirements for R&D, regulatory approval through the Therapeutic Goods Administration (TGA), clinical validation, and distribution networks create barriers. However, advances in AI‑powered diagnostics and miniaturization are enabling niche entrants focused on specialized endoscopic applications to access the market.

Threat of Substitutes – Low

Traditional open surgery and non‑invasive imaging techniques represent partial substitutes, but the advantages of endoscopic procedures including reduced recovery time, minimally invasive interventions, and earlier detection of abnormalities make them increasingly preferred by both patients and healthcare providers.

Competitive Rivalry – High (Healthy)

The market features intensifying competition among global and domestic endoscopy device manufacturers, with companies differentiating through technological innovation, clinical efficacy, and after‑sales support. Australian hospitals and specialized clinics are using state‑of‑the‑art instruments to stay on the cutting edge of surgical care.

Request for Sample Report: https://www.imarcgroup.com/australia-endoscopy-devices-market/requestsample

MARKET GROWTH DRIVERS

Rising Prevalence of Gastrointestinal and Chronic Diseases

Australia is experiencing a rising incidence of gastrointestinal disorders and chronic conditions, notably colorectal cancer, which is projected to be the fourth most commonly diagnosed cancer in 2024 with an estimated 15,542 new cases. This growing burden significantly fuels demand for endoscopic procedures, particularly colonoscopies, which are essential for early detection and monitoring. Lifestyle‑related illnesses such as obesity and acid reflux are also on the rise, prompting increased use of minimally invasive diagnostic tools. In tandem with an increasingly aged population and increased rates of chronic disease, hospitals and clinics are investing proactively in new endoscopy technologies to advance diagnostic precision and patient outcomes. National programs such as the Bowel Cancer Screening Program reinforce the trend by advocating regular screening and preventive care, driving adoption of endoscopic products throughout urban locations and regional health networks.

Technological Advancements in Endoscopic Equipment

The Australia endoscopy devices market is experiencing significant growth due to rapid technological innovation. Advances such as high‑definition imaging, three‑dimensional visualization, robotic‑assisted endoscopy, and AI‑powered diagnostics enhance the precision, safety, and efficacy of procedures. These developments allow earlier detection of abnormalities, reduced recovery time, and minimally invasive interventions, which are increasingly preferred by both patients and healthcare providers. To stay on the cutting edge of surgical care, Australian hospitals and specialized clinics are using these state‑of‑the‑art instruments. Ongoing collaborations between medical device companies and research institutions further propel market growth, promoting the local development and integration of advanced technologies.

Government Healthcare Support and Infrastructure Investment

The Australian government’s sustained investment in healthcare infrastructure and early diagnosis policies is a key driver of the endoscopy devices market. Programs like Medicare and the National Bowel Cancer Screening Program subsidize endoscopic procedures, improving accessibility and encouraging early detection. In 2024 alone, approximately 7,265 individuals aged 50–74 are projected to be diagnosed with bowel cancer, accounting for about 47% of all cases, highlighting the importance of screening initiatives. Public hospital funding supports the adoption of advanced surgical and diagnostic equipment, including modern endoscopy technologies. Additionally, regional and rural health programs are expanding access to care through mobile and tele‑endoscopy services.

AUSTRALIA ENDOSCOPY DEVICES MARKET SEGMENTATION

Segmentation analysis provides a detailed view of the Australia endoscopy devices market by category:

Type Insights: Endoscopes, Visualization Systems, Operative Devices, Accessories.

Application Insights: Gastrointestinal Endoscopy, Laparoscopy, Arthroscopy, Urology Endoscopy, Bronchoscopy, Others.

End Use Insights: Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Others.

Regional Insights: Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia.

COMPETITIVE LANDSCAPE

The competitive landscape of the Australia endoscopy devices market is dynamic, featuring global medical device manufacturers, specialised endoscopy companies, and emerging technology providers competing across traditional and AI‑powered diagnostic platforms. The market research report provides a comprehensive analysis of the competitive landscape, including market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant, with detailed profiles of all major companies provided in the full report. Investment opportunities exist in AI‑powered diagnostic systems, robotic‑assisted endoscopy platforms, high‑definition imaging solutions, and tele‑endoscopy services for regional and rural healthcare access.

REGIONAL ANALYSIS

Australia Capital Territory & New South Wales represents a critical demand centre, anchored by Sydney’s concentration of major hospitals, specialized clinics, and research institutions driving adoption of advanced endoscopy technologies.

Victoria & Tasmania benefits from Melbourne’s strong healthcare research ecosystem and government investment in digital health, supporting innovation in endoscopy diagnostics and AI‑powered systems.

Queensland sees rising demand driven by the state’s growing population and increasing healthcare infrastructure investment, supporting expanded access to endoscopic procedures.

Western Australia experiences steady growth supported by Perth’s expanding healthcare network and increasing adoption of minimally invasive surgical technologies.

Northern Territory & Southern Australia, though smaller in market share, are benefiting from mobile and tele‑endoscopy services improving access to care in regional and remote areas.

RECENT INDUSTRY DEVELOPMENTS

2025 Activity: The Australia endoscopy devices market continued its growth trajectory, driven by rising prevalence of gastrointestinal disorders, technological advancements in endoscopic equipment, and sustained government investment in healthcare infrastructure.

2025 Activity: Australian hospitals and specialized clinics continued to adopt high‑definition imaging, 3D visualization, and AI‑powered diagnostic systems to enhance procedural precision and patient outcomes.

2025 Activity: Regional and rural health programs expanded access to care through mobile and tele‑endoscopy services, improving screening and diagnostic capabilities in underserved areas.

Note: If you need any specific information that is not covered currently within the scope of the report, we will provide the same as a part of customization.

ABOUT US

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

CONTACT US

IMARC Group134 N 4th St., Brooklyn, NY 11249, USAEmail: sales@imarcgroup.comTel No: (D) +91 120 433 0800United States: +1 201 971 6302

Comments